Unlocking Alpha: Quantum Computing for Portfolio Optimization in the AI Era

In the relentless pursuit of superior returns and robust risk management, financial professionals are constantly seeking a competitive edge. The advent of quantum computing for portfolio optimization represents a groundbreaking frontier, promising to revolutionize how investment strategies are formulated and executed. This deep dive explores how the unparalleled computational power of quantum systems can tackle the most complex challenges in financial modeling, offering a glimpse into the future of asset management and investment decision-making. Prepare to understand how this transformative technology could redefine portfolio construction, risk assessment, and ultimately, your financial success.

The Evolving Landscape of Portfolio Optimization Challenges

For decades, portfolio managers have relied on sophisticated mathematical models and classical computing power to balance risk and return. Traditional approaches, such as Markowitz's Modern Portfolio Theory (MPT), Monte Carlo simulations, and various forms of quadratic programming, have served well within their computational limits. However, as markets become increasingly interconnected, volatile, and data-rich, the inherent limitations of classical methods are becoming starkly apparent.

Complexity and Scalability: Beyond Classical Limits

The core challenge in portfolio optimization lies in its combinatorial nature. As the number of assets in a portfolio grows, the number of possible combinations for asset allocation explodes exponentially. This "curse of dimensionality" quickly renders many real-world optimization problems intractable for even the most powerful supercomputers. Consider a portfolio with hundreds or thousands of assets; identifying the truly optimal allocation, especially when factoring in complex constraints like liquidity, transaction costs, and regulatory requirements, becomes an NP-hard problem. Classical algorithms often resort to approximations or heuristics, which, while practical, may not yield the globally optimal solution, potentially leaving significant "alpha" on the table. This is where quantum advantage begins to shine.

Limitations in Real-World Scenarios and Dynamic Markets

Classical models often struggle with the dynamic, non-linear relationships prevalent in financial markets. Market volatility, sudden shifts in correlations, and the impact of macroeconomic events introduce levels of uncertainty that are difficult to model accurately. Furthermore, the ability to perform real-time re-optimization in response to market fluctuations is severely limited by computational speed. Imagine needing to rebalance a global portfolio across multiple asset classes and geographies in milliseconds – a feat largely impossible with today's classical infrastructure. Traditional methods also find it challenging to incorporate multi-objective optimization, such as simultaneously optimizing for return, risk, environmental, social, and governance (ESG) factors, and liquidity constraints without significant computational compromise. This demand for more sophisticated and rapid solutions naturally points towards new computational paradigms.

Quantum Computing: A Paradigm Shift for Financial Modeling

Quantum computing leverages the peculiar laws of quantum mechanics to process information in fundamentally different ways than classical computers. Instead of bits that are either 0 or 1, quantum computers use qubits, which can exist in multiple states simultaneously, offering a dramatic increase in processing capability for specific types of problems.

Key Quantum Concepts for Financial Applications

- Qubits: Unlike classical bits, a qubit can represent a 0, a 1, or a superposition of both simultaneously. This enables quantum computers to explore many possibilities at once.

- Superposition: The ability of a qubit to be in multiple states at the same time allows quantum algorithms to process vast amounts of information in parallel, dramatically accelerating calculations for certain problems.

- Entanglement: When qubits become entangled, their states are linked, meaning the state of one instantly influences the state of another, regardless of distance. This powerful correlation is crucial for certain quantum algorithms to achieve computational speedups.

- Quantum Parallelism: Through superposition and entanglement, a quantum computer can effectively perform many calculations simultaneously, exploring a vast solution space much faster than a classical computer. This is particularly beneficial for optimization and simulation tasks inherent in financial modeling.

Why Quantum for Optimization Problems in Finance?

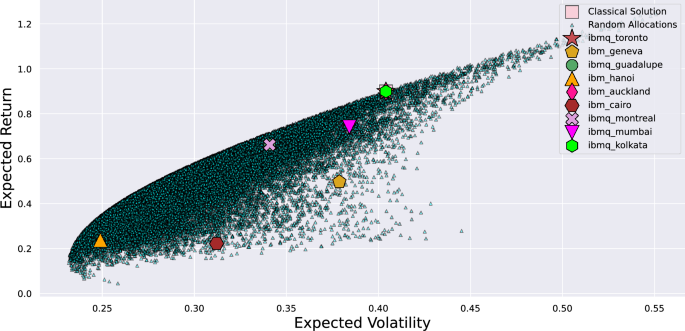

The inherent parallelism and unique properties of quantum mechanics make quantum computers exceptionally well-suited for solving complex optimization problems. Portfolio optimization, which seeks the best possible asset allocation given a set of constraints and objectives, maps perfectly onto problems that quantum algorithms are designed to tackle. By encoding financial variables (e.g., asset returns, correlations, risk factors) into qubits, quantum algorithms can explore an immense number of portfolio combinations simultaneously, identifying optimal or near-optimal solutions far more efficiently than classical methods. This capability extends beyond simple risk-return trade-offs to include highly intricate scenarios involving non-linear dependencies, real-time market data, and complex derivatives pricing. The promise of quantum algorithms lies in their potential to find global optima where classical methods might only find local ones.

Pioneering Quantum Algorithms for Portfolio Optimization

Several quantum algorithms are being actively developed and tested for their applicability in financial optimization. Each offers unique advantages for specific aspects of portfolio management.

Quantum Approximate Optimization Algorithm (QAOA)

QAOA is a hybrid quantum-classical algorithm designed to find approximate solutions to combinatorial optimization problems. For portfolio optimization, QAOA can be used to determine the optimal subset of assets to include in a portfolio or to solve for optimal weight distribution. It iteratively refines its solution by leveraging the quantum computer for the hard combinatorial part and a classical computer for optimizing the algorithm's parameters. This approach is particularly promising for problems like portfolio rebalancing or selecting assets under complex constraints, enabling more robust asset allocation strategies.

Quantum Annealing

Quantum annealing is a specialized quantum computing paradigm particularly adept at solving optimization problems by finding the lowest energy state of a system, which corresponds to the optimal solution. Companies like D-Wave Systems have built quantum annealers specifically for this purpose. In portfolio optimization, quantum annealing can be used to minimize portfolio risk (variance) subject to a target return, or to find the optimal allocation that minimizes transaction costs while achieving diversification goals. Its strength lies in efficiently exploring vast solution landscapes to pinpoint global minima, making it a powerful tool for complex risk management and investment strategies.

Variational Quantum Eigensolver (VQE)

VQE is another hybrid quantum-classical algorithm that can be used to find eigenvalues of matrices. In finance, this is highly relevant for tasks such as calculating the covariance matrix of asset returns, which is crucial for risk assessment and portfolio diversification. By accurately and efficiently calculating eigenvalues, VQE can help in identifying principal components of market risk or in optimizing complex derivatives pricing models, leading to more precise financial modeling and potentially higher returns on investment (ROI).

Quantum Machine Learning in Finance

Beyond direct optimization, quantum computing also offers significant potential for enhancing machine learning algorithms used in finance. Quantum machine learning (QML) can accelerate tasks like pattern recognition, anomaly detection, and predictive modeling, which are vital for forecasting market movements, identifying fraudulent activities, and building more intelligent trading strategies. When combined with portfolio optimization, QML could enable dynamic portfolio adjustments based on real-time market predictions, leading to truly adaptive and high-performance investment strategies. [internal link to 'Quantum Machine Learning in Finance']

Tangible Benefits of Quantum-Enhanced Portfolio Management

The integration of quantum computing into financial practices promises a multitude of benefits that could fundamentally alter the landscape of investment management.

Enhanced Diversification and Robust Risk Management

Quantum computers can process far more variables and constraints simultaneously, allowing for the construction of portfolios that are diversified not just across asset classes, but also across various risk factors, geopolitical exposures, and even environmental impacts. This leads to truly robust portfolios that are better insulated against market shocks and unforeseen events. By accurately modeling complex interdependencies, quantum-enhanced portfolio management can identify and mitigate risks that classical models might overlook, leading to more stable and predictable returns.

Faster Computation and Real-time Insights

The ability of quantum computers to perform calculations at unprecedented speeds means that portfolio rebalancing, risk assessments, and scenario analyses can be conducted in near real-time. This agility is critical in fast-moving markets, allowing managers to react swiftly to new information, seize fleeting opportunities, and adjust exposures before adverse conditions fully materialize. Imagine running thousands of Monte Carlo simulations in seconds, or re-optimizing a global portfolio across thousands of securities within minutes – this level of computational speed will empower truly dynamic investment strategies.

Discovering Non-Obvious Correlations and Alpha Opportunities

Classical correlation matrices often simplify relationships between assets. Quantum computing's ability to handle high-dimensional data and complex, non-linear interactions can uncover subtle, non-obvious correlations that are invisible to classical analysis. These hidden relationships might exist between seemingly unrelated assets, market indicators, or even alternative data sources. Discovering these nuanced connections can lead to novel diversification benefits and previously untapped sources of alpha, providing a significant competitive advantage in the quest for higher return on investment (ROI).

Optimizing for Multiple Objectives Simultaneously

Modern portfolio management is rarely about a single objective like maximizing return for a given risk. Investors increasingly demand portfolios optimized for multiple, sometimes conflicting, objectives: maximizing returns, minimizing risk, adhering to ESG criteria, ensuring liquidity, managing tax implications, and satisfying specific client mandates. Quantum optimization can simultaneously weigh and balance these diverse objectives, finding a more holistic and Pareto-optimal portfolio solution that satisfies a broader range of requirements, leading to truly customized and comprehensive financial solutions.

Practical Implementation & The Road Ahead

While the full potential of quantum computing is still emerging, financial institutions can already take actionable steps to prepare for and leverage this transformative technology.

Current State and Near-Term Applications: Hybrid Approaches

Today, quantum computers are still in their early "noisy intermediate-scale quantum" (NISQ) era. Full-scale, fault-tolerant quantum computers are years away. However, hybrid classical-quantum approaches are already viable. This involves using classical computers for the bulk of the data processing and problem setup, while offloading the computationally intensive, intractable optimization parts to quantum processors. This allows financial firms to gain experience with quantum algorithms, understand their limitations, and begin to develop quantum-ready software and talent. Pilot programs focusing on specific, high-value optimization problems, such as derivatives pricing or specific types of arbitrage, are excellent starting points.

Challenges and Roadblocks

- Hardware Maturity: Current quantum hardware is prone to errors (noise) and has limited qubit counts, restricting the complexity of problems that can be solved.

- Error Correction: Developing robust quantum error correction techniques is a major ongoing research area.

- Talent Gap: There's a significant shortage of professionals skilled in both quantum mechanics and financial engineering.

- Data Preparation: Translating complex financial data into a quantum-computable format (quantum encoding) is a non-trivial task.

- Cost and Accessibility: Access to high-performance quantum computers is currently limited and expensive, though cloud-based services are making it more accessible.

Actionable Steps for Financial Institutions

To capitalize on the future of quantum computing for portfolio optimization, proactive measures are essential:

- Investing in Talent & R&D: Begin building or acquiring a team with expertise in quantum information science, financial mathematics, and software development. Support internal research and development initiatives focused on quantum applications in finance. Consider sponsoring academic research or establishing quantum innovation labs.

- Pilot Programs & Partnerships: Start small with targeted pilot projects on specific, high-value optimization problems. Collaborate with quantum hardware providers, software developers, and academic institutions. Partnerships can provide access to cutting-edge technology and expertise without requiring massive upfront investments. Explore open-source quantum frameworks like Qiskit or Cirq.

- Data Preparation for Quantum: Understand the implications of quantum data encoding. Begin to assess and structure your financial data in ways that would be compatible with future quantum algorithms. This includes exploring techniques for feature engineering and data compression suitable for quantum processing.

- Stay Informed and Engage: Keep abreast of the rapid advancements in quantum technology. Participate in industry forums, conferences, and consortia dedicated to quantum finance. This proactive engagement will ensure your institution is well-positioned to adopt quantum solutions as they mature.

The journey towards widespread quantum adoption in finance will be incremental, but the competitive advantages for early adopters will be substantial. By strategically investing in quantum capabilities now, financial institutions can prepare to unlock unprecedented levels of efficiency, insight, and alpha in their portfolio management operations. [internal link to 'Future of Financial Technology']

Frequently Asked Questions

What is the primary advantage of quantum computing for portfolio optimization?

The primary advantage is its ability to solve highly complex, combinatorial optimization problems that are intractable for classical computers. Quantum computers can explore an exponentially larger number of possible solutions simultaneously, allowing for the identification of truly global optimal portfolios, factoring in more variables and constraints (like market volatility, transaction costs, and ESG factors) than ever before. This leads to more robust, diversified, and higher-performing investment strategies.

Is quantum computing ready for widespread portfolio optimization today?

While quantum computing shows immense promise, it is not yet ready for widespread, production-scale portfolio optimization across all financial institutions. Current quantum hardware is still in its early stages (NISQ era), characterized by limited qubit counts and susceptibility to errors. However, hybrid classical-quantum algorithms are being developed and tested, allowing for initial explorations and proof-of-concept projects. Financial institutions are advised to start investing in R&D, talent, and pilot programs to prepare for future adoption as the technology matures.

How does quantum computing handle risk management in portfolios?

Quantum computing significantly enhances risk management by enabling more sophisticated risk modeling. Algorithms like VQE can efficiently calculate complex covariance matrices, helping to understand asset correlations more accurately. Quantum annealers can optimize portfolios to minimize various risk metrics under multiple constraints. This allows for a deeper understanding of market volatility, better stress testing, and the ability to construct portfolios that are more resilient to unforeseen market conditions, going beyond traditional risk-return optimization to incorporate a broader spectrum of financial and non-financial risks.

What are the key quantum algorithms used in financial optimization?

Several key quantum algorithms are being explored for financial optimization. The Quantum Approximate Optimization Algorithm (QAOA) is used for combinatorial problems like asset selection and weight distribution. Quantum Annealing is highly effective for finding optimal solutions to complex constraint satisfaction problems, such as minimizing risk or maximizing return. The Variational Quantum Eigensolver (VQE) helps in calculating eigenvalues for tasks like covariance matrix analysis and derivatives pricing. These algorithms, often used in hybrid classical-quantum settings, form the backbone of quantum finance applications.

What skills are needed to apply quantum computing in finance?

Applying quantum computing in finance requires a multidisciplinary skill set. This includes a strong foundation in financial modeling, quantitative finance, and investment theory. Additionally, expertise in quantum mechanics, quantum information science, and quantum algorithm development is crucial. Proficiency in programming languages commonly used in quantum computing (like Python with quantum SDKs such as Qiskit or Cirq) is also essential. A blend of financial acumen and deep technical quantum knowledge will be key for professionals looking to leverage this emerging field.

0 Komentar